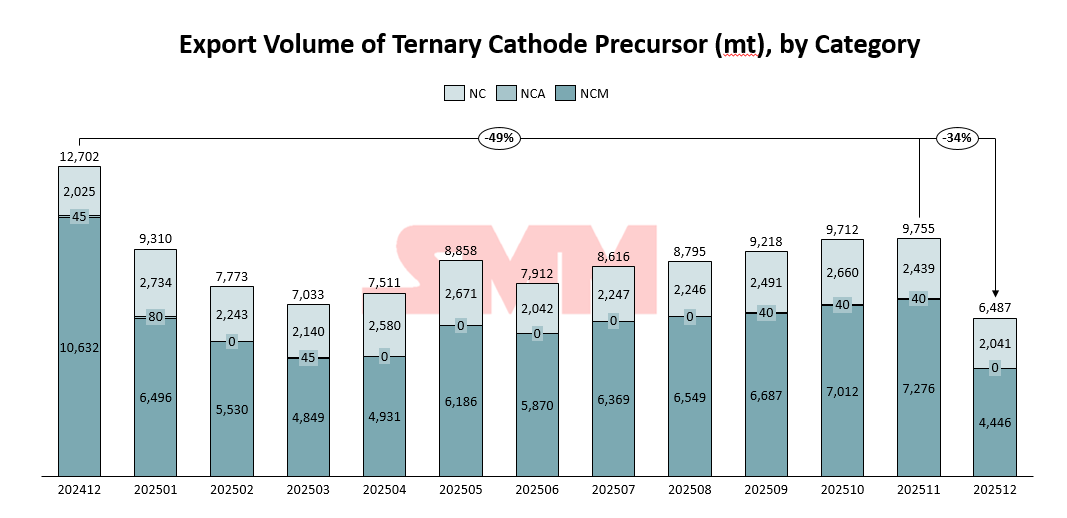

In December 2025, China's ternary precursor exports totaled 6,487 tons, marking a significant decline of 34% month-on-month and 49% year-on-year. By product type, NCM precursor exports were 4,446 tons, down 39% month-on-month, while NC precursor exports reached 2,041 tons, a decrease of 16%. No NCA product exports were recorded for the month.

By Country: Korea Remains Core Export Market, Diverging Demand in US and Europe

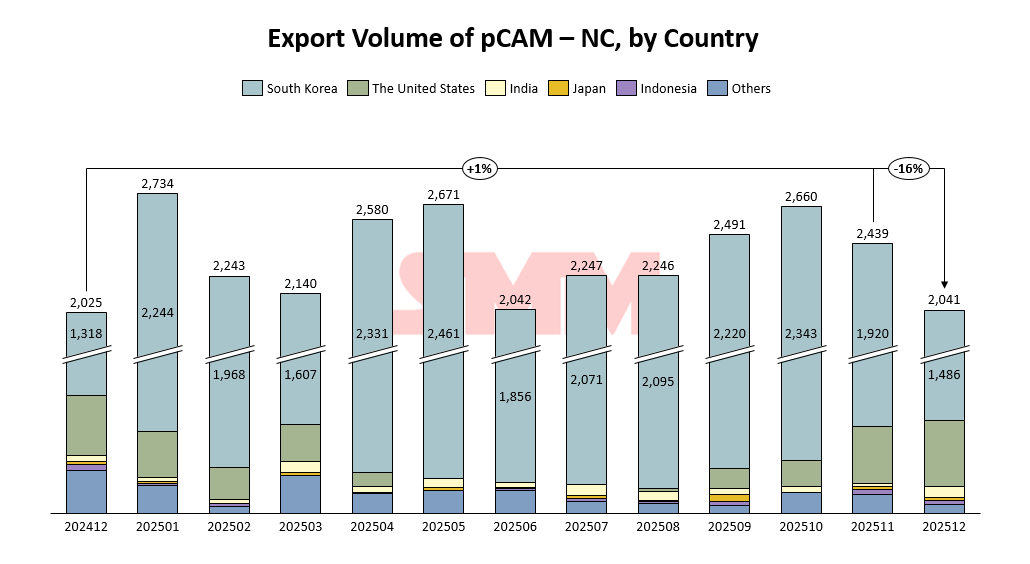

For NC precursors, South Korea maintained its position as China's primary export destination, with shipments of 1,486 tons in December, accounting for 73% of total NC exports. The United States ranked second with 391 tons.

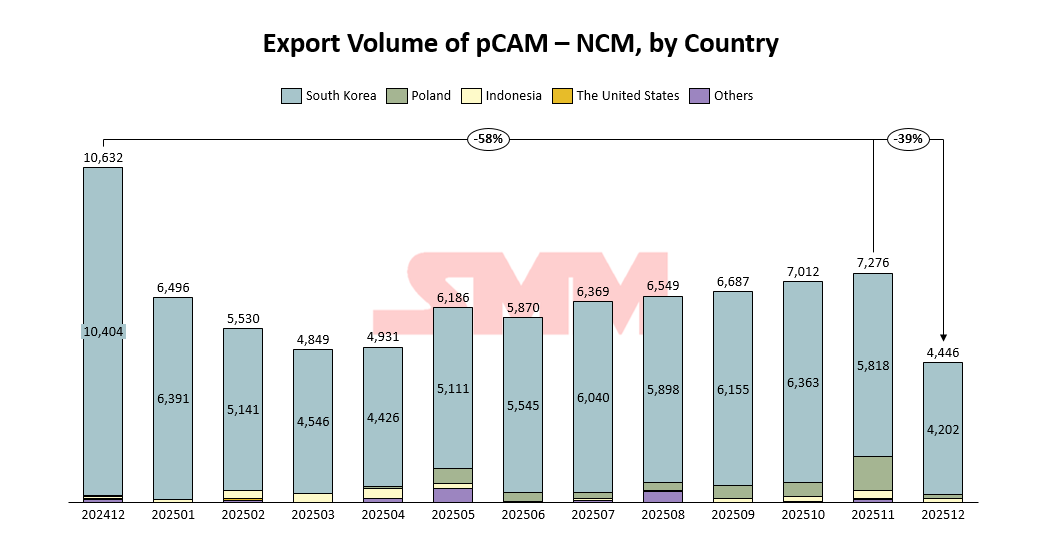

Exports of NCM precursors were also highly concentrated in South Korea, reaching 4,202 tons in December, constituting 95% of the total. The Polish market, which showed notable performance previously, experienced a sharp decline, plummeting from 1,087 tons in November to just 121 tons this month.

The sharp drop in precursor export demand at year-end was mainly driven by an overall weakening in overseas demand for ternary batteries. The US market, impacted by the phase-out of EV subsidies and adjustments to tariff policies, saw a notable decline in electric vehicle sales. This led to the cancellation of collaboration projects between some automakers, battery manufacturers, and leading Korean battery cell producers, which in turn affected Korean cathode material manufacturers' procurement of precursors. The likelihood of a favorable shift in US policy appears low. Several manufacturers have decided to switch originally planned ternary battery production capacity to LFP routes. Consequently, demand expectations for ternary materials in the US market remain cautious moving forward, and order prospects for Japanese and Korean battery cell makers targeting the US market are also not optimistic.

In contrast, positive signals persist in the European market. The European Commission's "Guidance Document on Price Undertakings for Chinese Electric Vehicles" issued on January 12 of this year, along with the German government's reinstatement of EV purchase subsidies around the same time, have somewhat alleviated pressure on Chinese automakers' exports and helped stabilize market confidence. As more overseas production bases of Chinese cathode material and battery enterprises gradually commence operations, ternary precursor exports to Europe are expected to achieve growth.

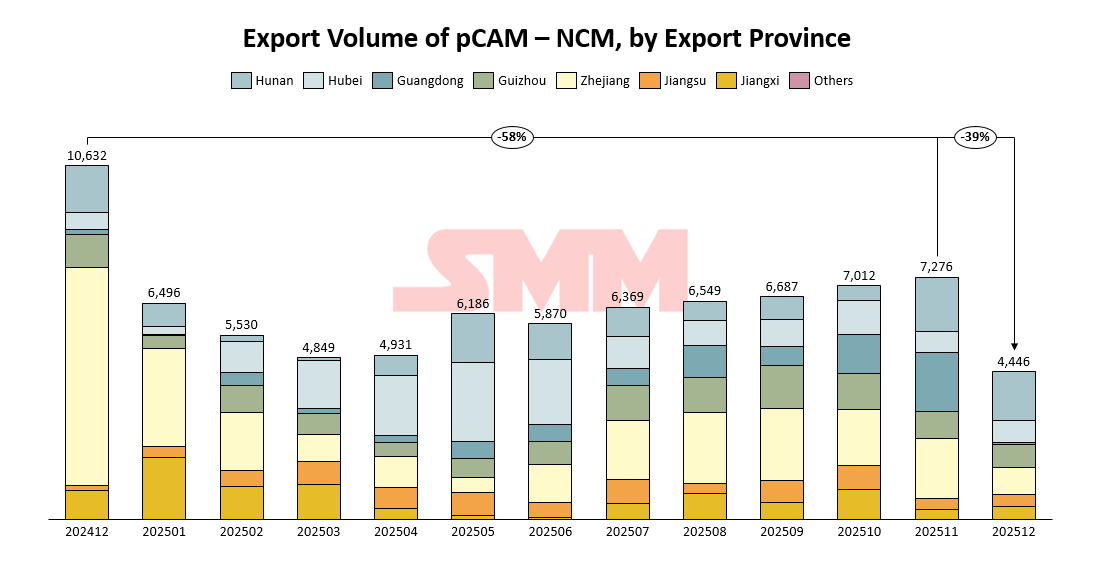

By Province: Hunan Maintains Lead, Notable Regional Fluctuations

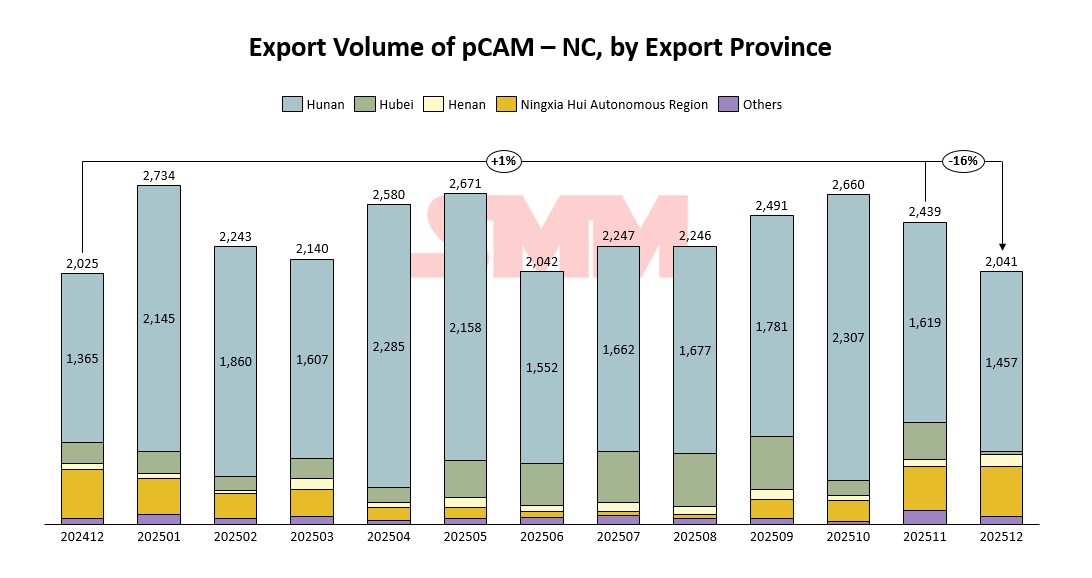

Analyzing the distribution by export province, Hunan continued to lead in NC precursor exports, shipping 1,457 tons in December, accounting for 71% of the total. The Ningxia Hui Autonomous Region ranked second with 408 tons, showing a slight month-on-month increase. Hubei Province experienced a significant drop, with exports falling from 301 tons in November to 24 tons.

For NCM precursors, Hunan was also the largest exporting province, with 1,477 tons exported in December, representing 33% of the total. Most provinces saw declines of varying degrees. Guangdong Province recorded a particularly sharp decrease, dropping from 1,770 tons in November to 61 tons. Zhejiang Province's exports fell from 1,818 tons to 807 tons.

Export Tax Rebate Cancellation: Short-term Pressure, Long-term Shift Towards Healthy Development

Export orders currently remain concentrated among a few leading domestic precursor enterprises. With the impending cancellation of the export tax rebate policy, the phenomenon of concentrated exports in the first quarter is expected to be prominent. In the long term, the phase-out of the export rebate policy is an inevitable trend in the industry's development. As the lithium battery industry transitions from rapid growth to a phase of slower adjustment, issues such as overcapacity and intense price competition have become increasingly prominent. Against this backdrop, policy adjustments can help steer industry competition back towards rationality.

Relying excessively on subsidies for profitability is not sustainable for the healthy long-term development of the industry. Although a larger issue may seem to be uneven profit distribution across different segments of the industrial chain, the overcapacity within the precursor sector itself is an undeniable fact. The gradual phasing out of supportive policies will, in the long run, benefit companies that possess genuine product competitiveness, technological advantages, well-established overseas layouts, and the capability to effectively navigate the risks associated with changes in international trade policies.